Basically there are two types of mortgage insurance available in the market, Mortgage Reducing Term Assurance (MRTA) and Mortgage Level Term Assurance(MLTA).

MLTA is a slight variation from MRTA and offers an alternative for a borrower who is looking for a life insurance which offers protection plus savings and in some policies returns on the premium.

In a nutshell, MLTA offer level/consistent protection, allow you to buy/sell property using the same MLTA protection & offer cash back and interest comparing to MRTA.

Also please note that most of the times, it is not compulsory to buy MRTA from the bank that you get the housing loan with, if the banker tells you so, do let me know

The table below shows the difference between MRTA and MLTA:

| MRTA | MLTA | |

| Purpose | Protection | Protection, Saving & Cash Value |

| Protection | Reducing Protection throughout the loan tenure. | Protection is leveled throughout the loan tenure. |

| Transferability | Non transferable on New Purchase or Refinance. Premium will increase while age increases. | Transferable. One MLTA can be attached to Any Loan. Transferable on New Purchase or Refinance. |

| Cash Value | Reducing Cash Value throughout the loan tenure. Normally is much lower than Premium, and drop to RM0 at the end of loan tenure. | Fixed Cash Value (Guaranteed) throughout the loan tenure. Policy Holder will get back the paid premium in the future. |

| Nomination | Beneficiary is bank | Beneficiary can be anyone. |

| Payment | Lump Sum Payment or financed into Mortgage Loan. | Payment Mode can be Annually, Semi Annually, Quarterly or Monthly. |

| Premium | Low | High |

| Example on premium* | One time RM1,186.34 | RM607.2 monthly or RM7,286.4 yearly or RM218,592 throughout the tenure |

| Example if there is no death or TPD* | At the end of tenure owner will received RM0 | At the end of tenure, owner will received RM218,592 |

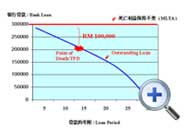

| Example if there is death or TPD** | Insurance company will pay the loan balance of RM372k to the bank & beneficiary will received the home. | Insurance company will pay the loan balance of RM372k to the bank & beneficiary will received the home plus RM100k cash. |

MRTA’s Disadvantages

| MLTA’s Advantages

|

Do call /SMS or Whatsapp me @ +60178865207 to know more about MLTA!

No comments:

Post a Comment