To retire or not to retire? I believe that is really not an option for most people. Retiring is only the privileged few, like, the 5% of the population who can really retire financially independent.

The majority of the people not only do not have the option to retire with financial independence, but they do not even have the option to retire at all. So, why is that the case?

We have to take a look at the problem in this equation. Let me illustrate.

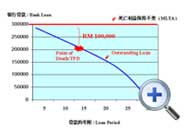

According to our Malaysian latest mortality rate, meaning how long Malaysians live, it has been said that we live to about 75 years old. We are not talking about now, so let’s take it further, about 20 to 30 years later although Malaysians will certainly live longer. Let’s say we retire from life at 85.

We can separate our life phases in to these two distinct phases called:

- Accumulation phase – This is from when you are 25-55, or your working years.

- Consumption phase, which is from 55-85 years old.

Do you see the problem? We have thirty years of working and thirty years of not working, meaning we will be consuming our savings. It simply means that each year of our working life, we will be actually saving for each year of our retirement years. At this point you cannot afford not to miss a years of savings because for each year of saving that you miss, you may not have enough for your retirement.

There’s another problem: How much do we save while we are working? Assuming all of you here are employees and you have EPF. If you have EPF you put aside 11% while your employer tops up another 12%. So, you get 23% going in to your EPF every month.

However, when you retire, you would need, I believe, a minimum of 50% of your last drawn salary. However your last drawn salary may be your highest income, assuming RM10,000. So, you would need about 50% of that, which would be RM5,000. Imagine why this is a problem. You need 50% but you are only putting 23% while you are working. That means there is a shortfall of 27% or more than a quarter.

Do you know the statistics from EPF? It says 50% of retirees spend their entire EPF savings within 5 years. This is the problem. It is scary, yeah.

It is never too late to start planning for your retirement. The earlier you do so, the more advantages you have. As with any investment activities, diversification is still the key.

Pick up investment books and get to know more investment products in the market would be a great start. Knowledge is power, especially when it comes to finding the best investment in Malaysia.

In this case, hopefully you will build a profitable investment portfolio for your pension money. While you are at it, don’t forget to check out Hong Leong Cash Promise, the latest buzz in financial industry.

Feel free to contact me @ 0178865207 to know more about HLA Cash Promise!